Why does Dave recommend that you invest in mutual funds for at least five years? Because short-term investing is how most people lose money — and Dave Ramsey has seen it happen thousands of times.

His entire investing philosophy is built around one core truth: the stock market rewards patience and punishes panic.

Mutual funds spread your risk across hundreds of companies, compound your returns over time, and historically recover from every single downturn.

Five years is not an arbitrary number. It is the minimum time horizon backed by decades of market data that separates disciplined wealth-builders from frustrated, reactive investors.

Who Is Dave Ramsey and Why Does His Advice Matter?

Dave Ramsey is one of the most widely followed personal finance voices in America. He hosts a nationally syndicated radio show, founded Ramsey Solutions, and has authored multiple bestselling books including The Total Money Makeover and Baby Steps Millionaires.

He built his following by teaching everyday people — not Wall Street professionals — how to get out of debt and build lasting wealth. His advice is simple, repeatable, and behavior-focused.

Over three decades, Ramsey Solutions has helped millions of Americans pay off debt and reach millionaire status using his Baby Steps framework. His investing philosophy is the heart of that wealth-building system.

The Core of Dave’s Investing Philosophy

Dave’s approach to investing is not complicated. He sums it up in five principles that anyone can follow.

Get out of debt first. Dave insists that you pay off all consumer debt and build a 3–6 month emergency fund before investing a single dollar.

Invest 15% of your income. Once the foundation is solid, Baby Step 4 directs you to put 15% of your household income into tax-advantaged retirement accounts like a 401(k) or Roth IRA.

Use mutual funds exclusively. Dave does not recommend individual stocks, cryptocurrency, options, or ETFs. His only recommended investment vehicle is growth stock mutual funds.

Think long-term. He repeatedly says that investing is a marathon, not a sprint. Time in the market always beats timing the market.

Work with a professional. He recommends connecting with a SmartVestor Pro — a vetted financial advisor — to guide specific decisions.

Why Does Dave Recommend That You Invest in Mutual Funds for at Least Five Years?

This is the question at the heart of his entire investing framework. The five-year minimum is not a soft suggestion — it is a hard rule grounded in how the market actually behaves.

The stock market is volatile in the short term. In any given year, the market can drop 20%, 30%, or even more. But over five-year rolling windows, the historical likelihood of a positive return increases dramatically.

Dave has watched countless investors panic-sell during downturns and lock in losses that they would have recovered if they had simply waited. The five-year minimum forces investors to think like owners, not speculators.

If you cannot commit to five years, Dave says you should not be investing that money in mutual funds at all.

Market Volatility and Why Time Fixes It

The stock market does not move in a straight line. It rises, falls, and recovers in cycles that can feel terrifying in the moment but look mild in hindsight.

Consider some of the most alarming market drops in recent history. The 2008 financial crisis saw the S&P 500 drop roughly 57% from peak to trough. Investors who sold at the bottom locked in catastrophic losses. Investors who held on saw a full recovery within five years.

The same pattern played out in the 2020 COVID crash, which dropped markets nearly 35% in a matter of weeks — and then fully recovered in just over five months.

Dave’s five-year rule provides a buffer that protects investors from making the worst mistake in investing: selling low out of fear.

| Market Crash | Peak Drop | Time to Full Recovery |

|---|---|---|

| Dot-com Bust (2000–2002) | ~49% | ~7 years |

| Financial Crisis (2007–2009) | ~57% | ~5.5 years |

| COVID Crash (2020) | ~34% | ~5 months |

| 2022 Bear Market | ~25% | ~2 years |

The lesson is consistent: every crash recovered. Every investor who stayed the course came out ahead.

The Power of Compound Interest Over Five Years

Compound interest is what makes the five-year rule so powerful. Dave calls compound growth the “secret weapon” of ordinary investors.

Here is a simple way to understand it. When your investment earns a return, that return gets reinvested. The following year, you earn returns on your original investment plus the previous year’s gains. Over five, ten, or twenty years, this snowball effect becomes enormous.

Dave uses 10–12% as his benchmark average annual return based on the historical performance of growth stock mutual funds. Most financial planners use 7–10% for conservative projections.

| Monthly Investment | Years Invested | At 10% Return | Total Contributed |

|---|---|---|---|

| $500 | 5 | ~$38,000 | $30,000 |

| $500 | 10 | ~$103,000 | $60,000 |

| $500 | 20 | ~$382,000 | $120,000 |

| $500 | 30 | ~$1,131,000 | $180,000 |

The difference between five and thirty years is not just time — it is the exponential curve of compounding kicking into high gear. The longer you stay invested, the more of your final balance comes from growth rather than your own contributions.

What Are Mutual Funds and Why Does Dave Prefer Them?

A mutual fund pools money from many investors to purchase a diversified collection of stocks. A professional fund manager selects and manages the holdings based on the fund’s investment objectives.

Dave prefers mutual funds over individual stocks for one primary reason: diversification. When you buy one stock, your entire investment is tied to one company’s performance. When you buy a mutual fund, your money is spread across dozens or hundreds of companies.

If one company goes bankrupt inside a mutual fund, it barely moves the needle. If you own only that stock, you lose everything.

Dave also prefers actively managed mutual funds over index funds — a stance that some financial experts debate. His reasoning is that a skilled fund manager, picking the right companies, can outperform the broader market over time.

He specifically recommends funds with at least a 10-year track record of strong, consistent returns — ideally outperforming the S&P 500.

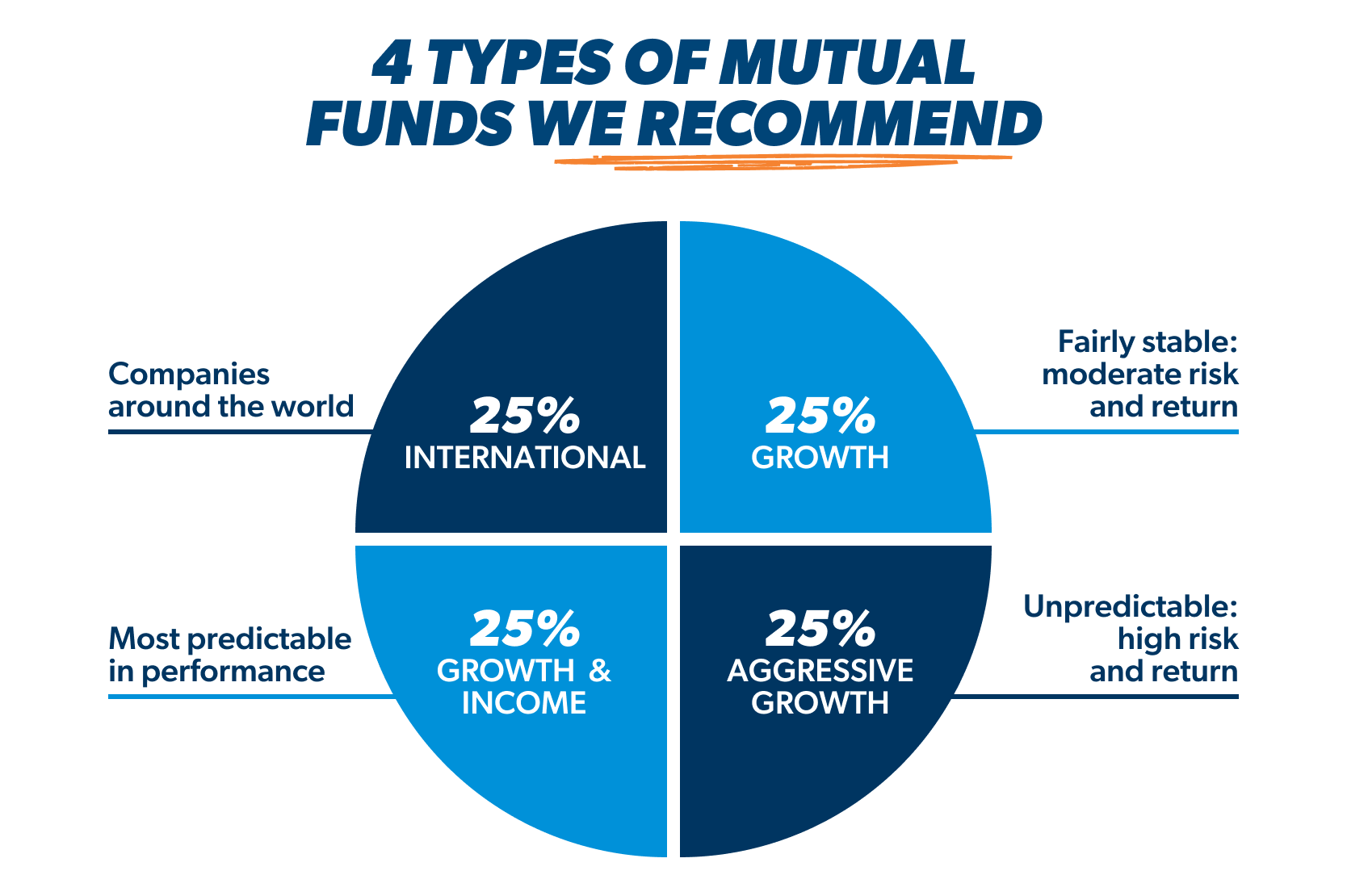

Dave’s Four Types of Mutual Funds: The 25/25/25/25 Rule

Dave does not just say “buy mutual funds.” He is very specific about which types to buy and in what proportion. He recommends splitting investments equally — 25% each — across four categories.

This split gives investors exposure to different market segments, company sizes, and geographic regions, reducing the risk that any one category’s poor performance will drag down the entire portfolio.

| Fund Type | What It Invests In | Also Called | Risk Level |

|---|---|---|---|

| Growth and Income | Large, stable U.S. companies with dividends | Large-cap or blue-chip funds | Lower |

| Growth | Mid-sized U.S. companies growing steadily | Mid-cap or equity funds | Moderate |

| Aggressive Growth | Smaller, fast-growing companies | Small-cap or emerging market funds | Higher |

| International | Large non-U.S. companies globally | Foreign or overseas funds | Moderate-Higher |

Growth and Income Funds: The Stable Foundation

Growth and income funds invest in large, well-established American companies. Think of household names that have been around for decades and regularly pay dividends.

These funds are the calmest in the portfolio. They do not spike dramatically upward, but they also do not collapse sharply downward. Companies like Coca-Cola, Procter & Gamble, and Johnson & Johnson are the kind of stocks typically found in this category.

Dave calls them “big, boring companies” — and he means that as a compliment. Boring, steady, and reliable is exactly what a retirement portfolio needs as its foundation.

Growth Funds: The Middle Ground

Growth funds invest in medium-sized U.S. companies that are actively expanding. These are companies that have moved past the startup phase but still have significant room to grow.

They carry more volatility than large-cap funds but offer stronger growth potential. Dave sometimes refers to these as “Goldilocks” funds — not too risky, not too conservative, but just right for the core of a long-term portfolio.

Mid-cap funds typically follow the performance of companies with market capitalizations between $2 billion and $10 billion.

Aggressive Growth Funds: The Wild Card

Aggressive growth funds invest in smaller, faster-moving companies. These can include startups, younger technology companies, and rapidly expanding businesses in emerging sectors.

The potential upside is higher than any other fund type. The volatility is also higher. A single aggressive growth fund could drop 30% in a bad year and gain 50% in a great year.

Dave includes this category because, over a long time horizon, the higher growth potential of small-cap companies contributes meaningfully to overall portfolio performance. The five-year minimum matters especially here — short-term holders of aggressive growth funds are most likely to panic and sell at the wrong moment.

International Funds: Geographic Diversification

International funds invest in large companies outside the United States. This provides diversification beyond U.S. economic conditions, interest rates, and political events.

Dave is careful to distinguish between international funds — which invest exclusively in non-U.S. companies — and global or world funds, which mix U.S. and foreign stocks. He recommends the former, not the latter, because global funds often contain significant U.S. exposure that duplicates what the other three fund types already provide.

Adding international exposure means that if the U.S. market underperforms for a period, gains in international markets can help offset those losses.

Baby Step 4: Where Mutual Fund Investing Begins

Dave’s mutual fund recommendation does not exist in isolation. It is specifically tied to Baby Step 4 of his 7 Baby Steps framework.

| Baby Step | Action |

|---|---|

| Baby Step 1 | Save $1,000 as a starter emergency fund |

| Baby Step 2 | Pay off all debt except the mortgage (debt snowball) |

| Baby Step 3 | Build a fully funded emergency fund of 3–6 months |

| Baby Step 4 | Invest 15% of household income in retirement accounts |

| Baby Step 5 | Save for kids’ college fund |

| Baby Step 6 | Pay off the home early |

| Baby Step 7 | Build wealth and give generously |

Baby Step 4 is where mutual funds come in. Dave says you should not invest in mutual funds until Steps 1 through 3 are complete. The reasoning is behavioral as much as financial.

If you have consumer debt and market volatility strikes, you are far more likely to panic and withdraw your investments — exactly the short-term behavior the five-year rule is designed to prevent.

The 15% Rule: How Much to Invest

Dave recommends investing exactly 15% of your gross household income into retirement accounts. Not 10%, not 20% — 15%.

He views this as the sweet spot that allows consistent retirement wealth-building while also leaving room to pursue other Baby Steps simultaneously, like paying off the mortgage and funding a college account.

For a household earning $70,000 per year, 15% is $10,500 annually — or $875 per month going into mutual funds inside a 401(k) or Roth IRA.

Dave’s recommended account priority is:

- Contribute to your 401(k) up to the employer match — that is free money

- Max out a Roth IRA ($7,000 in 2026 for most filers)

- Go back to the 401(k) for any remaining portion of the 15%

Why Dave Chooses Roth IRA for Most Investors

Dave strongly prefers the Roth IRA for most investors because of its tax structure. With a Roth, you invest after-tax dollars and your money grows completely tax-free. Withdrawals in retirement are also tax-free.

For most people in their working years — especially those who expect to be in a higher tax bracket at retirement than they are today — the Roth IRA is the superior vehicle.

The Roth also has no required minimum distributions, meaning you are not forced to withdraw money at any specific age. This makes it ideal for long-term, hands-off investing aligned with the five-year philosophy.

Picking the Right Mutual Funds: Dave’s Criteria

Dave does not recommend specific mutual fund tickers. But he does give clear criteria for what a good fund looks like:

Track record of at least 10 years. He wants funds that have survived multiple market cycles — not funds that only launched during a bull market.

Consistent outperformance of the S&P 500. The fund should have a history of beating the benchmark index, not just matching it.

Professional management. Dave believes skilled fund managers add value. He is not a fan of index funds, though this is a contested position among financial experts.

Reasonable fees. While Dave does not obsess over expense ratios, he acknowledges that outrageously high fees erode returns. He will pay a commission for quality management.

The Dollar-Cost Averaging Advantage

One reason the five-year minimum is so effective is that it aligns perfectly with dollar-cost averaging — the practice of investing a fixed amount at regular intervals regardless of market conditions.

When markets are down, your fixed monthly contribution buys more fund shares. When markets are up, it buys fewer. Over time, this smooths out your average purchase price and reduces the risk of investing a large sum right before a downturn.

Dave is a strong advocate for this approach. He says that the investors who build the most wealth are simply the ones who never stop — they invest every month, in every market condition, for decades.

Common Mistakes Dave Says to Avoid

Dave has seen every investing mistake in the book. Here are the most common ones he warns against:

Starting too late. Even a five-year delay in beginning to invest costs you significantly due to lost compounding time.

Stopping during downturns. The worst time to stop investing is when the market is falling. Those are the months when your contributions buy the most shares at the lowest prices.

Chasing hot investments. Cryptocurrency, meme stocks, single company bets — Dave says these are speculation, not investing. They have no place in a retirement portfolio.

Withdrawing early. Early withdrawals from a 401(k) or IRA trigger a 10% penalty plus income taxes. This destroys the compounding you have spent years building.

Investing while in debt. High-interest debt grows faster than most investments. Paying off consumer debt before investing is always the mathematically superior move.

What Critics Say About Dave’s Mutual Fund Advice

No financial philosophy is without critics, and Dave’s is no exception. Here are the most common arguments made against his approach — and what defenders say in response.

| Criticism | Dave’s Position / Defense |

|---|---|

| Index funds beat active funds 85%+ of the time long-term | A carefully selected active fund with a 10+ year track record can still outperform |

| S&P 500 has outperformed his 4-fund portfolio recently | His portfolio was designed for diversification, not maximum return chasing |

| 12% return assumption is too optimistic | Historical S&P 500 average is ~10% pre-inflation; 12% is possible over long periods |

| ETFs are cheaper and often more tax-efficient | Dave values professional management and long-term holding over fee minimization |

| No bonds in portfolio increases volatility | For long-term investors, stocks consistently outperform bonds over 20+ years |

The honest takeaway: Dave’s approach is excellent for behavioral discipline and simplicity. For advanced investors, adjustments may improve returns. But for most everyday Americans, the approach works.

Real Results: What Following Dave’s Plan Looks Like

Dave’s radio show regularly features callers who have followed his Baby Steps and built significant wealth. He calls people who reach millionaire status “Baby Steps Millionaires.”

Research from Ramsey Solutions studying 10,000 millionaires found that the vast majority built their wealth through consistent, boring investing — primarily through employer-sponsored retirement accounts and mutual funds — not through inheritance, luck, or risky bets.

The number one factor? They never stopped investing, even when markets fell.

That conclusion validates exactly what the five-year rule is designed to accomplish: keeping investors in the market long enough for compounding to do its work.

How to Start Following Dave’s Mutual Fund Strategy in 2026

If you want to apply Dave’s approach starting today, here is a clear action plan:

Step 1 — If you have consumer debt, tackle it first using the debt snowball method. List debts smallest to largest and attack them one at a time.

Step 2 — Build a $1,000 emergency fund, then complete Baby Steps 1 through 3 before touching your investment account.

Step 3 — Once debt-free with a full emergency fund, open a Roth IRA or contribute to your employer’s 401(k).

Step 4 — Choose one fund from each of Dave’s four categories — growth and income, growth, aggressive growth, international. Split contributions 25% to each.

Step 5 — Set up automatic monthly contributions so the investing happens without requiring discipline every month.

Step 6 — Do not check your balance daily. Do not panic when markets fall. Do not change your strategy based on headlines.

Step 7 — Review your fund choices annually with a SmartVestor Pro to ensure they still meet the 10-year track record and performance criteria.

Frequently Asked Questions (FAQs)

Why does Dave recommend that you invest in mutual funds for at least five years?

Because the stock market is volatile short-term but historically positive long-term. Five years gives your investment enough time to recover from downturns and benefit from compound growth.

What are the four types of mutual funds Dave recommends?

Dave recommends splitting investments equally across growth and income, growth, aggressive growth, and international funds — 25% in each category.

Does Dave recommend index funds or actively managed mutual funds?

Dave recommends actively managed mutual funds with a strong 10-year track record, not index funds. This is one of his more debated positions among financial experts.

What return does Dave expect from mutual funds?

Dave uses 10–12% as his benchmark average annual return based on the historical performance of growth stock mutual funds over long periods.

Should I invest in mutual funds if I still have debt?

No. Dave says to pay off all consumer debt and build a full emergency fund before investing. Debt interest typically grows faster than early-stage investment returns.

What account should I use to invest in mutual funds Dave’s way?

Dave recommends using a Roth IRA first (after getting any 401(k) employer match), then going back to the 401(k) for the remainder of your 15% contribution target.

How much of my income should I invest in mutual funds?

Dave recommends investing exactly 15% of your gross household income into retirement accounts as part of Baby Step 4.

What happens if I invest in mutual funds for less than five years?

Short-term investing exposes you to market downturns without enough time to recover. Dave says if you cannot commit to five years, do not put the money in mutual funds.

Is Dave Ramsey’s mutual fund strategy right for everyone?

It is an excellent starting framework for most everyday investors. Those with advanced financial knowledge, higher risk tolerance adjustments, or specific tax situations may benefit from additional tailoring with a financial advisor.

What is dollar-cost averaging and why does Dave recommend it?

Dollar-cost averaging means investing a fixed amount every month regardless of market conditions. It removes emotion from investing, reduces average purchase cost over time, and is central to Dave’s consistent, long-term approach.

onclusion

Why does Dave recommend that you invest in mutual funds for at least five years? Because wealth is not built in a day, a month, or even a year — it is built through decades of patient, consistent investing that gives compound interest time to work its magic.

Dave Ramsey’s mutual fund strategy is not complicated, and that is precisely its strength. Four fund types. Fifteen percent of your income.

A five-year minimum commitment. Tax-advantaged accounts. No panic selling. No market timing. No speculative bets.

For millions of Americans who have followed this framework, the result has been real, lasting financial security. The market has recovered from every single crash in history.

The investors who stayed the course recovered with it — and came out richer on the other side.

Dave’s five-year rule is not a limitation. It is the foundation that everything else is built on.