Why is it important to know the tax implications of giving away money or an inheritance? Because one uninformed decision can cost your family thousands of dollars in avoidable taxes.

In 2026, with major changes under the One Big Beautiful Bill Act now in effect, the rules around gift taxes, estate taxes, and inherited assets have shifted significantly.

Understanding these rules protects both the giver and the recipient.

The 2026 Tax Landscape Has Changed Everything

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, permanently reshaped the rules around giving money and inheritance. This is the most important legislative update for estate planning in years.

The federal estate and gift tax exemption has increased to $15 million per individual in 2026, up from $13.99 million in 2025. For married couples, this means up to $30 million can transfer free of federal gift, estate, and generation-skipping transfer (GST) tax.

The top federal estate and gift tax rate still sits at 40% for any amount above the exemption. This rate makes knowing the tax implications of giving away money or an inheritance critically important for anyone with a growing estate.

What Is the Gift Tax and Why Does It Matter

The gift tax is a federal tax on the transfer of money or property from one person to another without receiving something of equal value in return. The IRS applies gift tax rules to prevent people from dodging estate taxes by giving everything away while alive.

If you give more than the allowed annual exclusion, you must file IRS Form 709 to report it. Failure to file can lead to penalties, audit risks, and costly complications for your estate plan.

The gift tax is typically paid by the giver, not the recipient. This is a common misconception that leads to poor planning decisions.

Annual Gift Tax Exclusion 2026: The $19,000 Rule

The annual gift tax exclusion for 2026 remains at $19,000 per recipient. This means you can give up to $19,000 to any number of individuals each year without triggering a gift tax return or reducing your lifetime exemption.

Married couples can combine their exclusions through a process called gift splitting. This allows a married couple to give $38,000 per recipient per year without any gift tax consequences.

If you have three adult children, a married couple can give each one $38,000 annually for a total of $114,000 per year in tax-free wealth transfers. Done consistently over years, this is a powerful estate reduction tool.

| Gift Tax Exclusion | 2025 | 2026 |

|---|---|---|

| Annual Exclusion Per Recipient | $19,000 | $19,000 |

| Annual Exclusion (Married Couple) | $38,000 | $38,000 |

| Lifetime Exemption Per Individual | $13.99 Million | $15 Million |

| Lifetime Exemption (Married Couple) | $27.98 Million | $30 Million |

| Top Gift/Estate Tax Rate | 40% | 40% |

| Annual Exclusion to Non-Citizen Spouse | $190,000 | $194,000 |

The Lifetime Gift and Estate Tax Exemption Explained

The lifetime exemption is the total amount you can give away during your life and at death before owing any federal gift or estate tax. For 2026 this is $15 million per person.

Any gift above the $19,000 annual exclusion eats into your lifetime exemption. For example, if you give your child $100,000 in 2026, the first $19,000 is excluded and the remaining $81,000 reduces your lifetime exemption from $15 million to $14,919,000.

Starting in 2027 the exemption will be adjusted annually for inflation, providing long-term certainty for estate planners. This is permanent law under the OBBBA, with no sunset provision like the previous TCJA rules.

Why Is It Important to Know the Tax Implications of Giving Away Money or an Inheritance at the State Level

Federal law is just one layer of the tax puzzle. Many states impose their own estate taxes, inheritance taxes, or both, often with much lower exemption thresholds than the federal level.

Twelve states and the District of Columbia impose state estate taxes, with rates ranging from 12% to 35%. Oregon taxes estates above $1 million, while New York’s threshold for 2026 is $7.35 million.

Six states impose inheritance taxes: Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania. These taxes apply to the beneficiary receiving the assets, not the estate itself, and rates vary based on the relationship to the deceased.

| State Tax Type | States That Have It | Typical Threshold |

|---|---|---|

| State Estate Tax | 12 states + DC | $1M to $7.35M+ |

| State Inheritance Tax | 6 states | Varies by state |

| Both Estate and Inheritance Tax | Maryland | Varies |

| No State Estate or Inheritance Tax | ~32 states | N/A |

If you own property in multiple states, each state’s rules apply to the property located there. This is why people with real estate in several states need to coordinate multi-state estate planning with a qualified attorney.

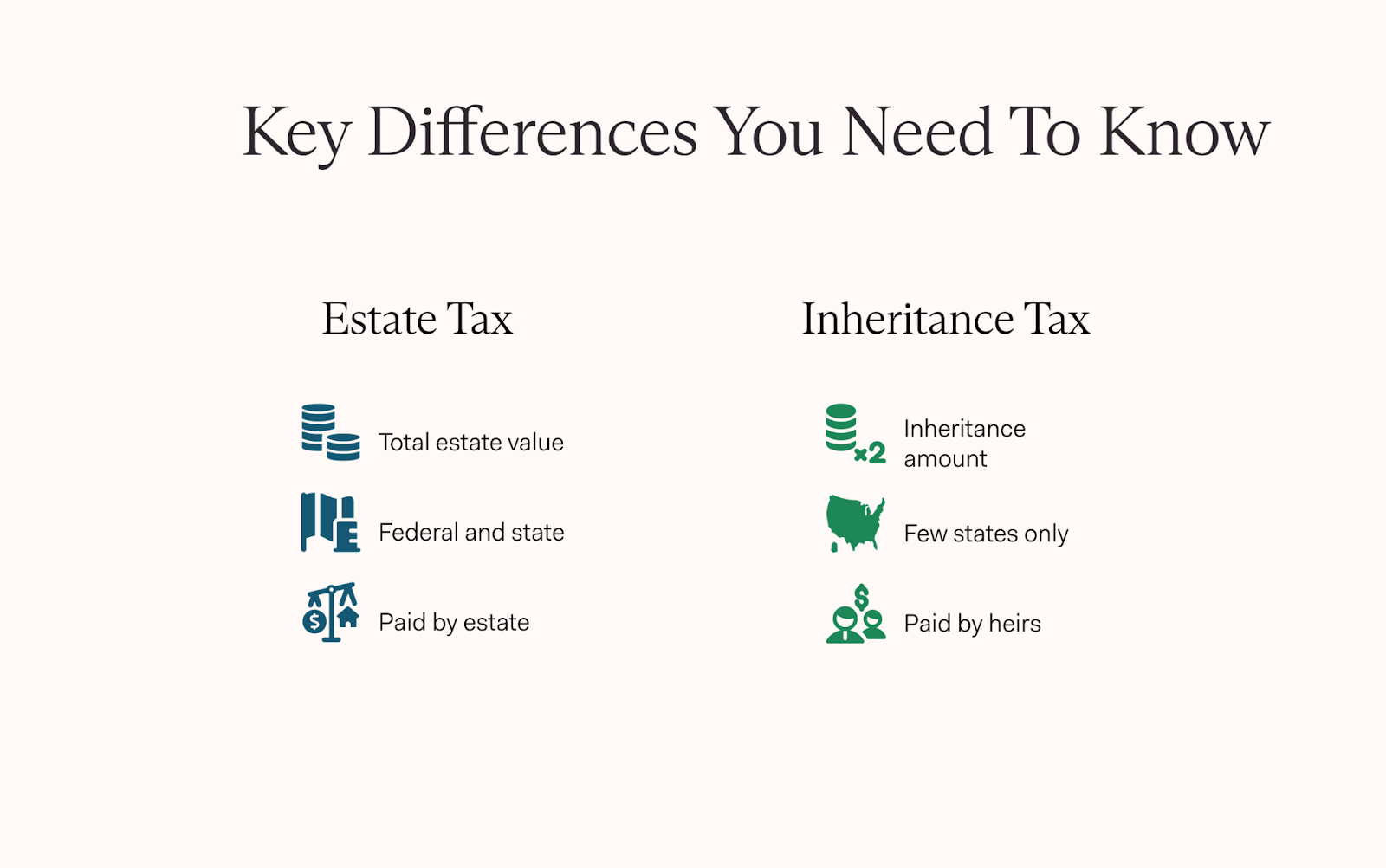

Estate Tax vs. Inheritance Tax: Key Differences

These two terms are often confused but they work very differently. Understanding both is central to knowing why it is important to know the tax implications of giving away money or an inheritance.

The estate tax is a tax on the total value of the deceased person’s estate before distribution. It is paid by the estate itself, reducing what beneficiaries ultimately receive. The federal estate tax only applies to estates above $15 million in 2026.

The inheritance tax is a state-level tax paid by the person receiving the inheritance. The tax rate often depends on how closely related the beneficiary is to the deceased. Spouses are typically exempt, while distant relatives or non-relatives pay higher rates.

| Feature | Estate Tax | Inheritance Tax |

|---|---|---|

| Who Pays | The estate | The beneficiary |

| Federal Level | Yes ($15M exemption in 2026) | No federal inheritance tax |

| State Level | 12 states + DC | 6 states |

| Rate Basis | Total estate value | Relationship to deceased |

| Typical Rate | Up to 40% (federal) | 0% to 18%+ (state) |

Capital Gains Tax on Inherited Assets and the Step-Up in Basis

Capital gains tax is one of the most misunderstood parts of inheritance planning. When you inherit an asset like real estate or stocks, the cost basis is typically adjusted to the fair market value on the date of the original owner’s death. This is called the step-up in basis.

The OBBBA preserved the step-up in basis rule for 2026. This means heirs can sell inherited assets at current market value without owing capital gains tax on appreciation that occurred during the deceased’s lifetime.

For example, if your parent bought a property for $200,000 decades ago and it is worth $900,000 when they pass away, your cost basis becomes $900,000. If you sell it for $900,000 shortly after inheriting it, you owe zero capital gains tax on that $700,000 gain.

This creates an important planning decision. Highly appreciated assets are often better passed at death to capture the step-up, rather than gifted during life where the recipient takes on the original low cost basis.

Gifting During Life vs. Leaving an Inheritance: The Tax Trade-Off

Knowing why it is important to know the tax implications of giving away money or an inheritance means understanding the trade-off between lifetime gifts and inherited assets.

Lifetime gifts remove assets from your taxable estate and shift future appreciation out as well. If you give $10,000 in stock and it grows to $50,000, that entire $50,000 is out of your estate. However, the recipient inherits your original low cost basis and may owe capital gains tax when they sell.

Leaving assets at death gives heirs the step-up in basis benefit, eliminating embedded capital gains. But those assets remain in your estate and may be exposed to estate tax if your estate is large enough.

The right answer depends on your specific asset types, estate size, state of residence, and the recipient’s tax situation. A qualified estate planning professional can model both scenarios for you.

Inherited IRAs and Retirement Accounts: Special Tax Rules

Retirement accounts come with their own set of tax rules that make inheritance planning even more complex. Understanding these rules is a key reason why it is important to know the tax implications of giving away money or an inheritance.

When you inherit a traditional IRA or 401(k) from someone other than your spouse, you generally must take required minimum distributions (RMDs) and distribute the full account within 10 years of the original owner’s death. All distributions from pre-tax accounts are taxed as ordinary income in the year you take them.

Inherited Roth IRAs work differently. Roth accounts have already been taxed, so qualified withdrawals are generally tax-free. However, the 10-year rule still applies for most non-spouse beneficiaries.

Withdrawals from inherited traditional IRAs in high-income years can push beneficiaries into higher tax brackets, increasing their overall tax burden significantly. Timing distributions strategically across the 10-year window can reduce this impact.

| Inherited Account Type | Tax on Distributions | Distribution Rule |

|---|---|---|

| Traditional IRA (non-spouse heir) | Ordinary income tax | 10-year rule applies |

| Roth IRA (non-spouse heir) | Generally tax-free | 10-year rule applies |

| 401(k) – Traditional (non-spouse heir) | Ordinary income tax | 10-year rule applies |

| Inherited IRA (spouse) | Ordinary income | Can roll into own IRA |

| Inherited Roth (spouse) | Generally tax-free | More flexible options |

Reporting Requirements: IRS Form 709 and What Triggers It

One of the most practical reasons why it is important to know the tax implications of giving away money or an inheritance is the IRS reporting obligation. Many people don’t realize that large gifts must be formally reported even if no tax is due.

IRS Form 709 is required whenever you give any individual more than $19,000 in a single calendar year. This includes cash, real estate, stocks, cryptocurrency, art, cars, and any other property with measurable market value.

Gifts that do not count toward the annual exclusion and do not require reporting include direct tuition payments made to a qualifying educational institution, direct medical payments made to a medical provider, gifts to your U.S. citizen spouse, and gifts to qualifying charities.

Failing to file Form 709 when required can result in interest, penalties, and complications during estate settlement. The IRS has six years to audit gift tax returns for substantial understatement of value, making accurate and timely filing essential.

Strategies to Minimize Tax When Giving Away Money or an Inheritance

Understanding the tax implications of giving away money or an inheritance allows you to use proven strategies that reduce tax liability legally and efficiently.

Annual gifting is the simplest tool. Giving $19,000 per recipient per year to as many people as you choose moves wealth out of your estate without touching your lifetime exemption. A couple with five children and ten grandchildren could gift $570,000 annually with zero gift tax impact.

Irrevocable trusts are powerful planning vehicles. An irrevocable trust removes assets from your taxable estate because you no longer legally own them. Common options include Spousal Lifetime Access Trusts (SLATs), Irrevocable Life Insurance Trusts (ILITs), and Grantor Retained Annuity Trusts (GRATs).

529 education accounts offer a unique super-funding strategy. You can contribute up to $95,000 per beneficiary ($190,000 for married couples) to a 529 plan in a single year and elect to treat it as five years of annual gifts. This supercharges educational savings while removing assets from your estate.

Charitable giving is another proven strategy. Donating to a qualified charity during your lifetime or through your estate reduces your taxable estate, potentially provides an income tax deduction, and supports causes you care about. Donor-advised funds are a flexible vehicle for this type of giving.

529 Plan Gifting: A Tax-Smart Way to Give

The 529 college savings account is one of the most underutilized tools for tax-efficient gifting. Contributions are made with after-tax dollars but grow tax-free and are distributed tax-free for qualified education expenses.

The five-year gift-tax averaging election, sometimes called superfunding, allows a one-time large contribution of up to $95,000 for an individual or $190,000 for a married couple per beneficiary without using any lifetime exemption.

For grandparents or parents wanting to reduce estate size while helping the next generation fund education, this strategy achieves both goals simultaneously. The contributed amount is removed from your estate immediately.

Trusts as a Tool for Tax-Efficient Wealth Transfer

Trusts are the backbone of sophisticated estate planning precisely because they address the tax implications of giving away money or an inheritance in multiple ways at once.

A revocable living trust does not reduce estate taxes because you retain control of the assets. However, it avoids probate, provides privacy, and simplifies asset distribution at death.

An irrevocable trust permanently removes assets from your estate. Any appreciation inside the trust also stays outside your estate. This is particularly powerful for high-growth assets like closely held business interests, concentrated stock positions, and real estate.

SLATs allow one spouse to gift assets to a trust for the benefit of the other spouse, removing assets from both spouses’ estates while maintaining indirect access. ILITs hold life insurance policies outside your estate, ensuring death benefit proceeds are not subject to estate tax.

| Trust Type | Estate Tax Benefit | Access to Assets | Best For |

|---|---|---|---|

| Revocable Living Trust | None | Full access retained | Probate avoidance |

| Irrevocable Trust | Yes — removes assets from estate | Limited or none | Large estate reduction |

| SLAT | Yes | Indirect via spouse | Married couples |

| ILIT | Yes — removes life insurance | Death benefit to heirs | Life insurance planning |

| GRAT | Yes — removes appreciation | Annuity payments returned | High-growth assets |

| Dynasty Trust | Yes — multi-generation | Trustee discretion | Multigenerational planning |

Generation-Skipping Transfer Tax: What It Is and Why It Matters

The generation-skipping transfer (GST) tax is a separate federal tax that applies when you transfer wealth to someone two or more generations below you, such as a grandchild or great-grandchild, either during life or at death.

For 2026 the GST tax exemption has also increased to $15 million per individual, aligned with the estate and gift tax exemption under the OBBBA. The top GST tax rate is 40%, the same as the estate and gift tax rate.

Without careful planning, a single asset can be taxed multiple times as it passes from grandparent to parent to grandchild. Dynasty trusts and direct skip arrangements are commonly used to transfer wealth across multiple generations while minimizing cumulative transfer taxes.

How Charitable Giving Reduces Your Tax Burden

Charitable giving sits at the intersection of generosity and tax efficiency, and it is a key strategy for anyone asking why it is important to know the tax implications of giving away money or an inheritance.

Donations to qualified charities reduce the value of your taxable estate dollar for dollar. If your estate is above the federal threshold, each dollar donated to charity directly reduces the amount subject to the 40% estate tax rate.

Qualified Charitable Distributions (QCDs) allow taxpayers over age 70½ to donate up to a certain amount annually directly from their IRA to a qualifying charity. This distribution counts toward your required minimum distribution but is excluded from taxable income.

Note that starting January 1, 2026, taxpayers can only deduct charitable contributions that exceed 0.5% of adjusted gross income as an itemized deduction. For a taxpayer with $300,000 in AGI, the first $1,500 in charitable donations will not generate a deduction. Larger bunched donations through a donor-advised fund may be more effective.

Portability: Preserving a Deceased Spouse’s Unused Exemption

Portability is one of the most valuable and frequently overlooked tax-saving tools available to married couples. It allows a surviving spouse to use any portion of the deceased spouse’s unused lifetime exemption.

For 2026 a deceased spouse could leave behind up to $15 million in unused exemption. If their estate was only $5 million, their surviving spouse can potentially claim the remaining $10 million and add it to their own $15 million exemption.

Portability must be elected on a timely filed estate tax return, IRS Form 706, due nine months after the date of death. Extensions are available but must be requested. Failing to file can permanently forfeit this valuable benefit.

The Impact of Poor Planning: Real-World Scenarios

Understanding why it is important to know the tax implications of giving away money or an inheritance is clearest when you look at what happens without proper planning.

Scenario one: a parent gives their adult child stock with a $50,000 original cost basis now worth $400,000. Without planning, the child takes on that low basis. When the child later sells the stock, they owe capital gains tax on $350,000 of gain. Had the parent held the stock until death, the step-up would have eliminated that tax entirely.

Scenario two: a grandparent gifts $200,000 to a grandchild without proper reporting or planning. The gift exceeds the annual exclusion by $181,000, reducing the grandparent’s lifetime exemption. If the grandparent’s estate is eventually above the exemption, this creates unintended estate tax exposure. A properly structured 529 superfund or trust could have achieved the same goal with far better tax efficiency.

Scenario three: a beneficiary inherits a $400,000 traditional IRA and withdraws it all in one year. The entire amount is added to their ordinary income, potentially pushing them into the 37% federal tax bracket. Spreading withdrawals strategically over the 10-year distribution window could have saved tens of thousands of dollars in income tax.

Working with Estate Planning Professionals

No article can substitute for personalized professional advice, and this is itself a core reason why it is important to know the tax implications of giving away money or an inheritance. The rules are complex, they vary by state, and they change with legislation.

Estate planning attorneys draft the legal documents needed to implement your strategy, including wills, trusts, powers of attorney, and healthcare directives. They ensure your assets transfer according to your wishes and in a legally valid manner.

Certified Public Accountants (CPAs) handle the tax reporting side, including gift tax returns (Form 709), estate tax returns (Form 706), and income tax planning for beneficiaries with inherited retirement accounts. A CPA who specializes in estate and trust taxation is an invaluable member of your planning team.

Financial advisors help integrate your estate plan with your investment strategy, ensuring your asset allocation, insurance coverage, and retirement income plan all work together to minimize taxes and maximize what passes to your heirs.

Key Tax Forms Associated with Gifting and Inheritance

Knowing the paperwork involved is a practical dimension of understanding the tax implications of giving away money or an inheritance. Several IRS forms govern this process.

Form 709 is the United States Gift and Generation-Skipping Transfer Tax Return. It must be filed any time you give more than $19,000 to any one person in a calendar year. It is due April 15 of the year following the year the gift was made.

Form 706 is the United States Estate and Generation-Skipping Transfer Tax Return. It is due nine months after the date of death and must be filed even if no estate tax is owed, if you want to elect portability for the surviving spouse.

Form 1041 is the income tax return for trusts and estates. It reports income earned by the estate during administration. Beneficiaries receive Schedule K-1 showing their share of income to report on their personal returns.

| IRS Form | Purpose | Filing Deadline |

|---|---|---|

| Form 709 | Report taxable gifts | April 15 of following year |

| Form 706 | Estate tax return | 9 months after death |

| Form 1041 | Trust/estate income tax return | April 15 (with extensions) |

| Schedule K-1 (1041) | Beneficiary income reporting | Issued by estate/trust |

Why 2026 Is a Critical Year for Estate Planning

The 2026 tax landscape represents one of the most favorable environments for wealth transfer in modern history. The $15 million federal exemption is now permanent, indexed for inflation, and paired with a $19,000 annual exclusion.

However, even with generous federal rules, state-level taxes can still bite. Twelve states have their own estate taxes, and six have inheritance taxes, many with thresholds well below $1 million. Residents of those states cannot rely on federal exemptions alone.

The 40% federal rate for estates above the exemption remains unchanged. For business owners, real estate investors, and individuals with concentrated stock positions, the estate tax remains a serious planning concern that demands proactive action now.

Summary: Why Knowing Tax Implications of Giving Money or Inheritance Is Non-Negotiable

Knowing why it is important to know the tax implications of giving away money or an inheritance is not just about avoiding taxes. It is about making intentional, informed decisions that honor your goals and protect your family.

Poor planning leads to unnecessary tax bills, family disputes, unintended consequences for beneficiaries, and missed opportunities to transfer wealth efficiently. Good planning, supported by knowledge of the current rules, achieves the opposite.

The 2026 rules give American families more opportunity than ever to transfer wealth tax-free. But the window is open only for those who understand how to use it. Staying educated, working with qualified professionals, and reviewing your estate plan regularly are the three most impactful actions you can take.

| Planning Strategy | Tax Benefit | Best Suited For |

|---|---|---|

| Annual Gifting ($19K per recipient) | Reduces estate, no gift tax | Everyone with assets to transfer |

| 529 Superfunding ($95K/$190K) | Estate reduction + education | Grandparents/parents |

| Irrevocable Trust | Removes assets and appreciation | High-net-worth estates |

| Charitable Donations | Estate reduction + deductions | Philanthropically inclined donors |

| Step-Up at Death | Eliminates embedded capital gains | Appreciated assets like real estate |

| Portability Election | Doubles surviving spouse’s exemption | Married couples |

| Inherited IRA Distribution Planning | Reduces income tax | Beneficiaries of retirement accounts |

Frequently Asked Questions (FAQs)

Why is it important to know the tax implications of giving away money or an inheritance?

It protects both giver and recipient from unexpected tax bills, ensures compliance with IRS rules, and helps you transfer wealth in the most efficient way possible.

What is the annual gift tax exclusion for 2026?

The annual gift tax exclusion is $19,000 per recipient in 2026, meaning you can give up to that amount to any individual without filing a gift tax return.

What is the federal estate tax exemption in 2026?

The federal estate and gift tax exemption increased to $15 million per individual ($30 million for married couples) in 2026 under the One Big Beautiful Bill Act.

Do recipients pay tax on money they receive as a gift?

No. The gift tax is typically paid by the giver, not the recipient. Recipients generally do not owe income tax on gifts received.

Is there a federal inheritance tax in 2026?

No. The United States does not impose a federal inheritance tax. However, six states have their own inheritance taxes that beneficiaries may owe depending on the state and their relationship to the deceased.

What is the step-up in basis and why does it matter for inheritance?

The step-up in basis adjusts the cost basis of inherited assets to their fair market value at the date of death, eliminating capital gains tax on appreciation that occurred during the original owner’s lifetime.

What happens if you give more than $19,000 to one person in 2026?

You must file IRS Form 709 to report the gift. The excess reduces your $15 million lifetime exemption. No gift tax is owed until your cumulative taxable gifts exceed the lifetime exemption.

What is portability in estate planning?

Portability allows a surviving spouse to use their deceased spouse’s unused federal estate tax exemption. It must be elected on a timely filed Form 706 estate tax return.

Are inherited IRAs taxed differently than regular IRAs?

Yes. Most non-spouse beneficiaries must withdraw the full inherited traditional IRA within 10 years, with all distributions taxed as ordinary income. Inherited Roth IRAs are generally tax-free if rules are met.

When should I consult an estate planning attorney about giving away money or an inheritance?

Consult a professional before making any gift above the annual exclusion, when structuring a trust, after a major life change, or when your estate is approaching a taxable threshold at the federal or state level.

Conclusion

Why is it important to know the tax implications of giving away money or an inheritance? Because the decisions you make today will directly shape how much of your wealth actually reaches the people you love.

The 2026 tax rules under the One Big Beautiful Bill Act offer historic opportunities with a $15 million federal exemption, a $19,000 annual gift exclusion, and the preserved step-up in basis for inherited assets. But these opportunities are only accessible to those who understand how to use them.

State-level estate and inheritance taxes, capital gains on gifted assets, inherited IRA distribution rules, and IRS reporting requirements all add layers of complexity that demand informed, proactive planning.

Whether you are giving now or planning for what you leave behind, working with an estate attorney, CPA, and financial advisor is the smartest investment you can make in your family’s financial future.